This blog is the first in a series of three snapshot articles on the effects of chip shortage on the industry: What impacts is it having? What changes are taking place in the industry, or even in politics, in attempts to guarantee supplies and ring-fence national or regional supplies? And finally, once plans are in place for second-sourcing, or alternative manufacturing, how does that affect design decisions, time-to-market and ultimately, profitability?

Access to chip supplies – hence to the manufacturing of chips – have become a strategic initiative for companies and nations alike. Lockdowns due to Covid-19 has arguably caused a lot of the ‘tailbacks’ seen in the industry. But while it’s been a catalyst, there are other factors at play and it’s making nation-states and regions start to evaluate the strategic importance of their chip supplies.

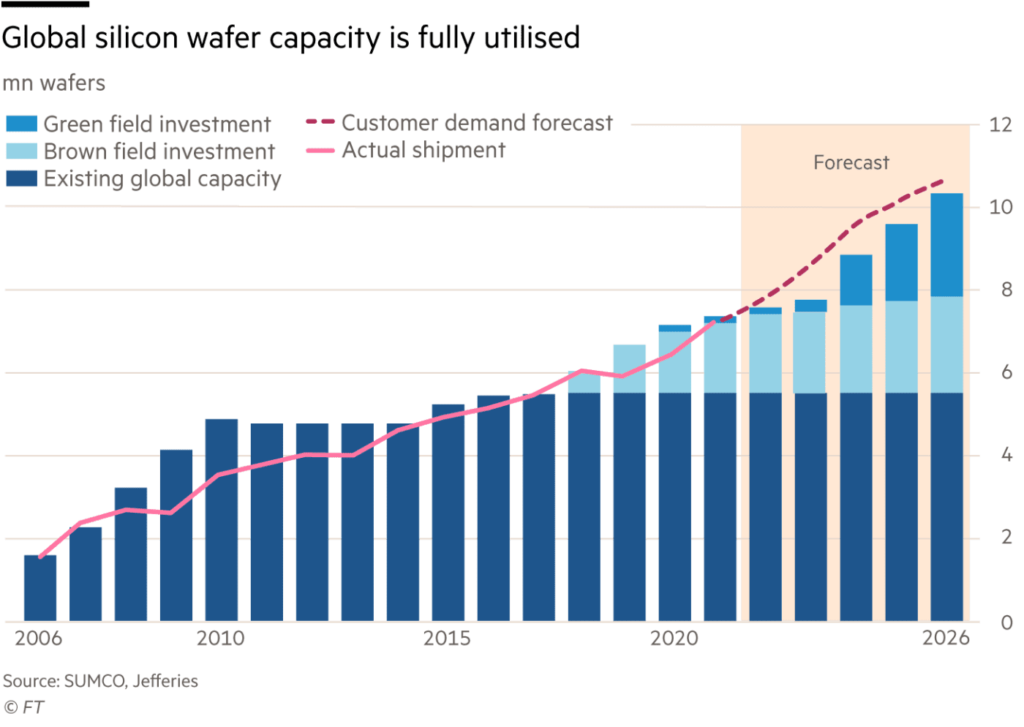

The fact is, in spite of problems with supply chain, or businesses affected in various ways due to Covid-19 lockdowns, demand has not dropped off, and shows no signs of scaling back. Quite the opposite.

In fact, we’ve seen in recent weeks, the risks of global conflict certainly affect supply and demand and can impact the industry in ways we’d never thought of, with the growing crisis in Ukraine set to affect the supply of palladium and scandium – some of the raw materials used in chip manufacturing:

But more generally, changes in the geopolitical climate are making chip companies consider and reconsider where they source or where they manufacture. US politics can discourage or stop companies from moving their manufacturing to China for example.

Global Wafers attempting to invest in Siltronic – but ‘stalling’ for what appears to be political reasons.

The big wafer fabs are rethinking their own strategies to both keep pace with the chip shortage and to fend off geopolitical risks that may affect their own supplies or access to their customers. Some of this is the Tier 1 chip makers extending their manufacturing, both to other parts of the world, or in the same region to simply increase their capacity.

But it’s not a quick fix: wafer fabs take a lot of money and typically at least three years to build and become operational.

In Europe, the $43bn EU chips act is targeting European self-sufficiency to raise its game – aiming for 20 percent of the global market by 2030. The act also is also designed to prioritise Europe’s own needs ‘in times of shortages’.

The second blog in this series will look at how companies are restructuring and where investment decisions are being driven by the risks of global chip shortages and these geopolitics pressures.